What is Perion?

An Ad Tech stock that I am bullish on. I have a TP of US$ 72 (127% upside).

What is Perion?

So what is Perion? Perion was listed on the NASDAQ from 2006. It is is a company that runs advertising and monetization solutions for both brands and publishers. Brands are typically people or organizations that want to advertise their product or services. Publishers are typically websites or apps that wants to display advertisements to monetize the traffic that lands on their website or applications. Perion has 2 main business segments namely Search Advertising and Display Advertising. Perion’s Search Advertising business forms ~41% of its business while Display Advertising form ~59% of its business. For the Search Advertising business, Perion makes money by directing search traffic from its various partners’ website to Bing and gets paid for it. For the Display Advertising Business, Perion displays advertisements on the website/platforms of its various partners and gets paid for it based on how many times the advertisement was seen or clicked. The advertisements displayed in this segment is typically more interactive (video, high impact advertising through the use of colourful, rich media).

Why I am positive on Perion Stock

Perion seems to be a good long due to 8 reasons.

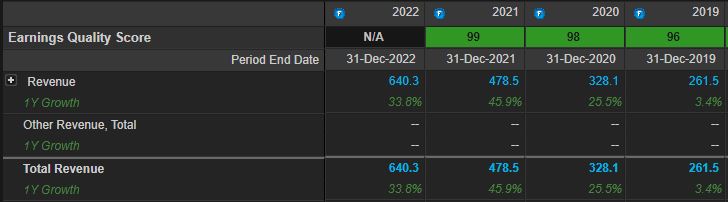

1) Perion had a history of mismanagement prior to 2017. New CEO was appointed in 2017 to turn the company around. CEO acquired companies to bring in new products to Perion. Products seem to be paying off currently with accelerating revenue growth. Revenue has accelerated from flattish growth in 2019 to strong growth in the past 3 years.

2) Under the Display Advertising Business, Perion is slowly expanding into connected TV (CTV) advertising (think of Disney+, Netflix,etc) since advertising budgets are shifting there. Perion acquired Vindazoo in 2021 to expand into the CTV space, allowing it to capture the growing advertising market there.

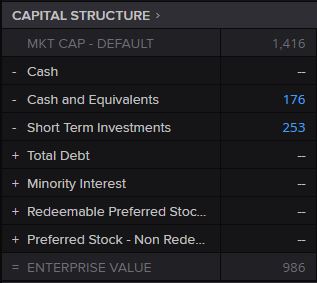

3) Perion has a sound balance sheet. Perion has 0 debt and >400m cash to acquire new companies to expand its product offering and to grow its revenue further. Considering the current macro-economic climate, Perion’s cash pile enables it to be nimble and to buffer for an economic downturn.

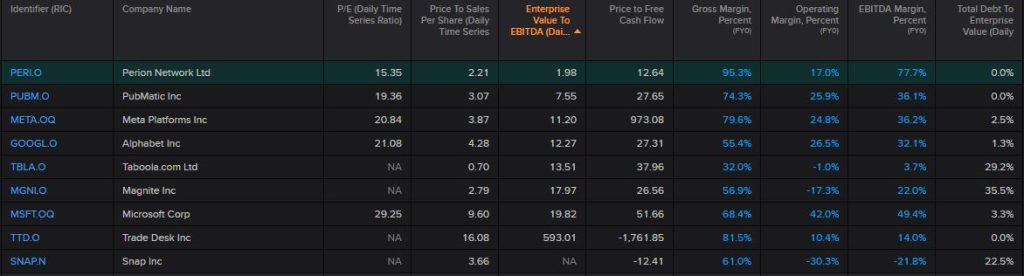

4) Perion’s valuation presents a high margin of safety. Based on any metric, Perion is valued at a discount compared to its peers despite growing revenue and earnings above the industry’s growth rate. If Perion continues to execute, the earnings multiple accorded to Perion should increase in line with its peers.

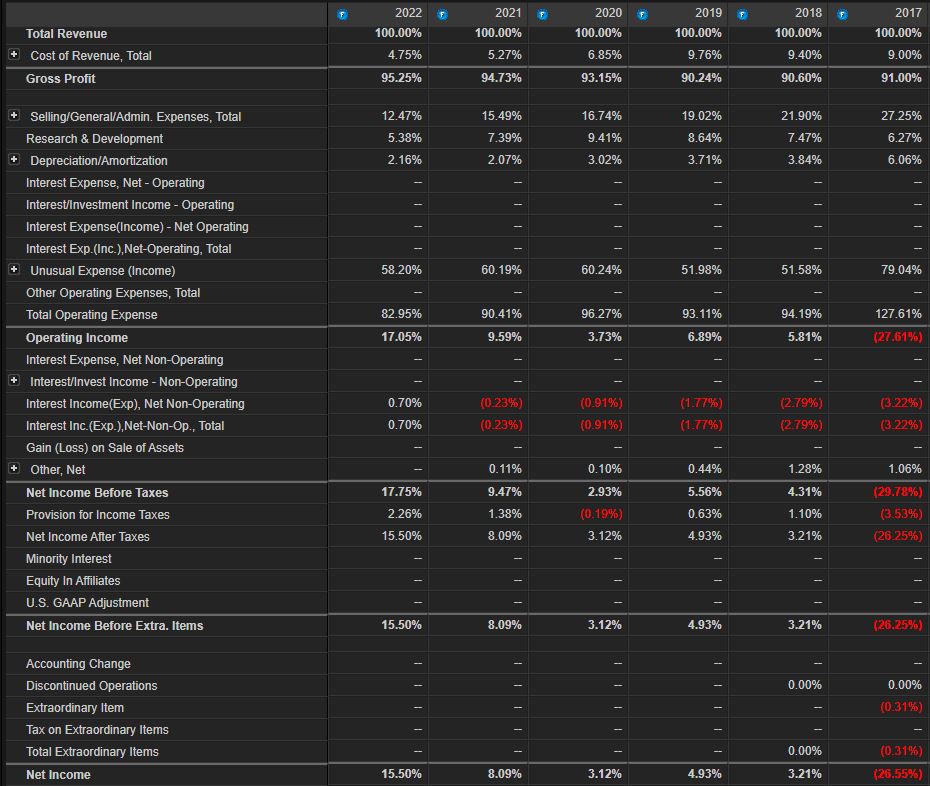

5) Perion has a proven business model. Perion has shown that it is able to attain operating leverage as its revenue grows. As shown below, Perion was able to grow its revenue faster than its expenses, resulting in its net income margin expanding from 3.13% in 2020 to 15.50% in 2022. With scale, I believe Perion to be able to grow its net income margin closer to 20%.

6) Perion is set to capitalise on Apple’s privacy changes. In 2022, Apple made some changes and made it harder for advertisers to target their advertisements. However, Perion was not affected as it uses a proprietary technology named SORT that did not rely on cookies for targeting. In fact, Perion’s technology was more effective compared to SORT in targeting, enabling it to win advertising budget from publishers

7) Perion’s subsidiary Code Fuel has been named Microsoft’s Global Supplier of the year, highlighting the expertise Perion has in the advertising industry.

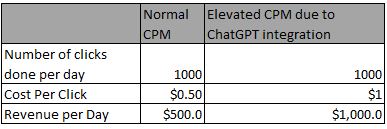

8) ChatGPT and its integration into Microsoft Bing is a wildcard. If the integration of Chat GPT into Bing enables Bing to win market share from Google, Perion could be a beneficiary. As more users utilize Bing, advertisers could bid more aggressively to advertise on Bing, driving the cost per impression or cost per click higher. Basically, advertisers have to pay more for advertising. This is a positive for Perion as Perion would be able to generate higher revenues on the same number of clicks. I have laid out a very simplistic table (not actual data) to illustrate this positive effect.

Furthermore, if ChatGPT successfully takes market share from Google, Microsoft estimates that for every 1% of market share gained, it will generate an additional $2 billion in revenue. As a partner of Microsoft, Perion will benefit significantly from this incremental revenue if it comes to fruition.

Considerations

1) Microsoft accounting for ~40% of Perion’s revenue. The concentration of Perion’s revenue around Microsoft will probably cause a valuation multiple discount when computing the target price of Perion. However, this is mitigated by Perion’s attempt to grow its digital advertising segment to diversify its revenue. Perion has attempted to grow it through acquisitions in that segment. More acquisitions can still be done to grow Perion’s digital advertising segment as Perion is sitting on ~400m worth of cash. Furthermore, in 2020, Microsoft extended its partnership with Perion to 2024 . The extension of the partnership gives Perion additional time to diversify its revenue further. As of today, Perion has been a valued partner of Microsoft, as evident from Perion winning Microsoft’s Global Supplier of the year. Thus, there is no reason to believe why Microsoft would not renew the partnership post 2024.

2) Slowing macro-economic conditions might cause advertisers to cut back on advertising budgets. Advertising giants like Google has already experienced a slowdown in advertising budgets; Google experienced a decline in revenue in its most recent quarterly report. This might cause Perion’s growth to taper. However, as of Perion’s latest earnings report, its revenue was still able to grow 32.7% Y/Y (despite Google’s negative growth rate), demonstrating its ability to grow above industry rates. Guidance from Perion’s management was also very positive with management expecting 14% Y/Y revenue growth for Perion despite poor guidance from Perion’s peers. In any case where Perion does not meet the guidance, I believe the valuation of Perion and Perion’s huge cash pile has greatly de risked the stock.

Target Price

I believe Perion to be worth $72/ share.

Below are my ballpark calculations for those who are interested.

Perion’s management has guided to about $150m EBITDA in 2023. Management has historically met or exceeded targets. Assuming a 15x multiple, Perion’s Enterprise Value should be worth $2.25B. Currently, Perion is trading at $31.7 as of writing and 986m Enterprise Value. An Enterprise Value of $2.25B implies approximately a 128% upside to current share price ($72 per share).

DISCLAIMER: The following writeup is for informational purposes only and should not be construed as a recommendation to buy, sell, or hold any securities. Investing in stocks involves risks, and past performance is not indicative of future results. The author and any related parties do not guarantee the accuracy or completeness of the information provided and shall not be held liable for any investment decisions based on the information presented. It is important to conduct your own research and seek professional advice before making any investment decisions.

To know about me click this link!